At a time when other smartphone companies are complaining about the poor economic climate and rising manufacturing costs, it seems Apple has found its own umbrella to enjoy the rain! Recent reports indicate that the iPhone sector is experiencing its best days, benefiting directly from Apple’s smart decision to keep retail prices for its phones stable, while the entire global smartphone market suffers from increasing pressure and a sharp rise in costs due to the ongoing shortage of memory chips.

Global Superiority During the Year’s Slowest Period

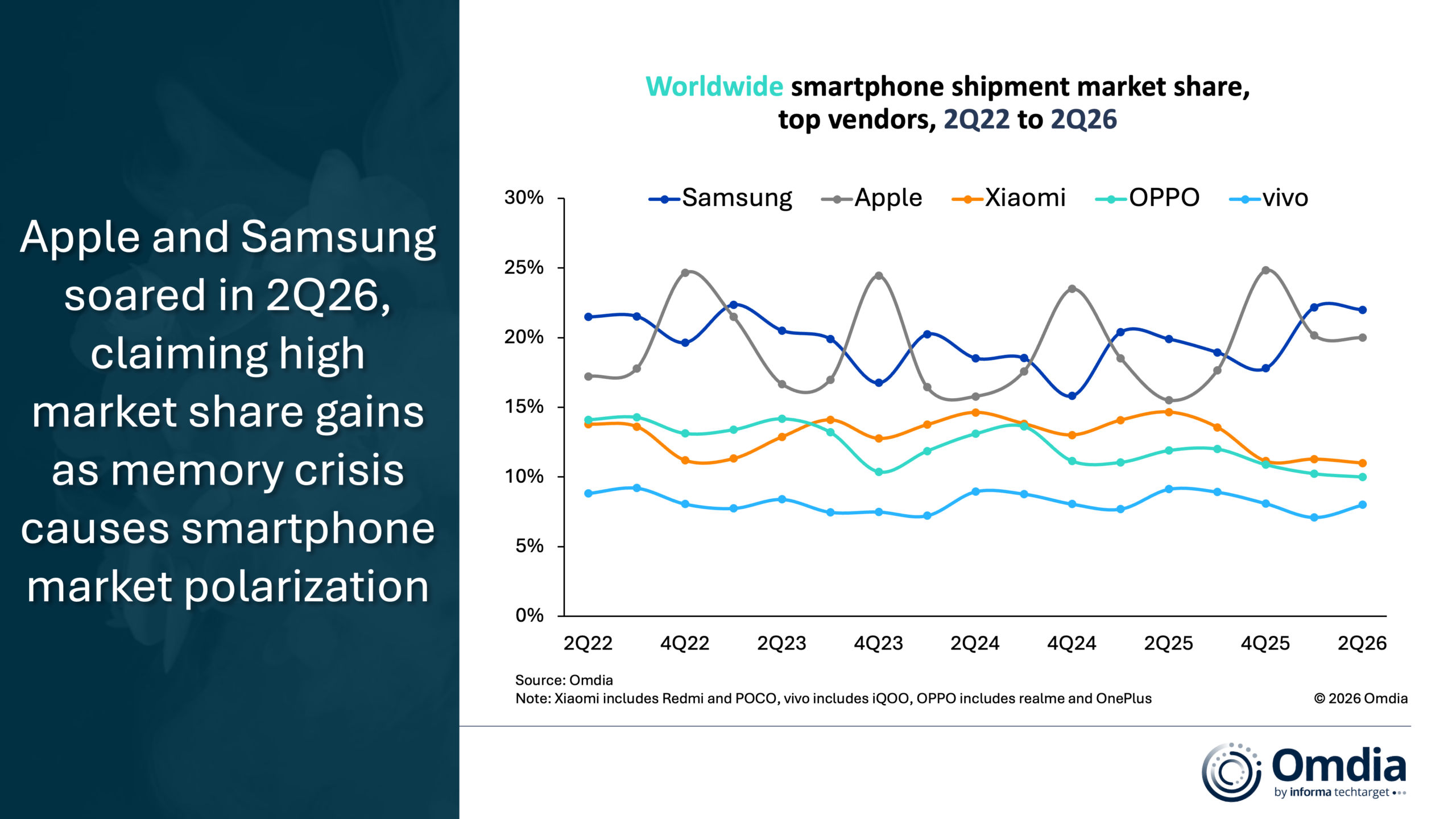

A recent report by the research firm Omdia showed that Apple succeeded in capturing a record market share of 20% of the global smartphone market during the second quarter of 2026. This achievement came as a major surprise to analysts, as it defies the general decline witnessed by the global market, which saw a 4% year-on-year drop in total shipments.

What makes this success even more exciting is the timing; the second quarter is traditionally known as the slowest season of the year for phone sales due to users anticipating new announcements in the fall. However, it seems the iPhone 17 family had a completely different opinion. According to Omdia, the secret behind these strong sales is partly due to Apple’s resilience and its refusal to increase retail prices for iPhones, despite having recently raised prices for Mac, iPad, and other company products.

The current global shortage of memory chips is due to the decision by major memory manufacturers to focus almost entirely on producing RAM and storage solutions for the booming Artificial Intelligence (AI) sector. As a result, major smartphone companies like Apple and Samsung are forced to pay exorbitant and ongoing prices to secure enough components to ensure their production lines continue without interruption.

Amidst this economic storm, Samsung was the only other company besides Apple to see growth in its global market share, capturing a 22% share. Meanwhile, Xiaomi maintained third place with 11%, followed by Oppo in fourth place with 10%, and Vivo in fifth place with an 8% share.

Invasion of the Chinese Dragon: Apple Soars Alone in the Chinese Sky

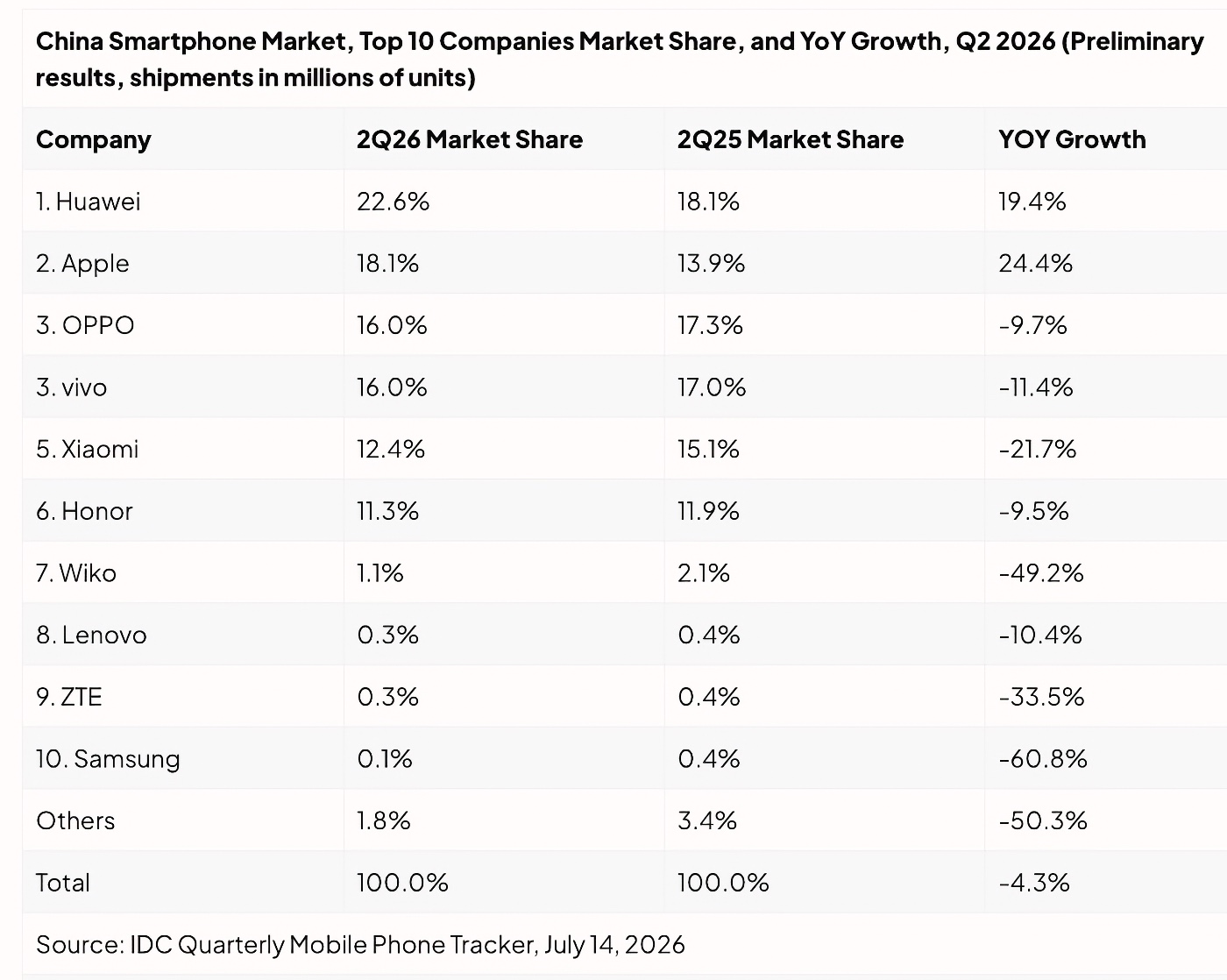

On the other side of the world, in one of the most competitive and difficult markets, Apple has achieved overwhelming success by all measures. Preliminary data released by the research firm IDC revealed that iPhone shipments in China jumped by a staggering 24.4% year-on-year during the second quarter of 2026. This record figure made Apple the fastest-growing brand in an already shrinking Chinese market!

It is worth noting that total smartphone shipments in China declined by 4.3%, settling at about 66 million units, marking the fifth consecutive quarter of decline and stagnation. Only Apple and Huawei (whose shipments grew by 19.4%) managed to swim against this downward current. Thanks to this strong performance, Apple’s market share in China rose to 18.1% compared to 13.9% in the same period last year, while the market leader Huawei’s share rose to 22.6%, whereas Xiaomi took the biggest hit among major brands with its shipments falling by 21.7%.

Strategy of Resilience Against the Price Storm

IDC’s analyses align with the Omdia report regarding the reason for this success; reports indicate that companies’ responses to rising manufacturing costs were the deciding factor in this battle. While most Android phone manufacturers began gradually raising their device prices since last March to cover high memory costs, Apple and its competitor Huawei chose to keep their prices stable without change to encourage users.

Furthermore, analysts believe that the rumors circulating about the possibility of Apple raising the prices of its upcoming phones have provided a strong incentive for hesitant users to rush to buy current iPhones before the anticipated price increase. According to analyst Arthur Guo from IDC, “This fear of future price hikes gave hesitant buyers an excellent reason to move forward with the purchase immediately without any delay.”

But will these rosy days last long? Future forecasts do not seem to promise complete comfort for companies. IDC expects the Chinese market to see no noticeable improvement in the near term; in fact, forecasts suggest a potential additional 20% year-on-year decline in the second half of 2026. Storage component prices are expected to continue putting pressure on company profit margins until 2027, with no real and comprehensive recovery for the market expected before 2028 or 2029.

Source:

Leave a Reply